In the business plan, the expected income and expenditure for the coming business year as well as the allocation to the maintenance reserve are planned. The figures are based on empirical values, price increase rates and absolute costs (which are already available in exact amounts at the time of preparation). The business plan contains only the costs for the administration and maintenance of the common property and costs that are usually settled via the community, such as water, waste disposal, heating costs, insurance, etc. The business plan also includes the costs for the maintenance reserve.

A distribution key is specified for each item in the business plan. The declaration of division specifies which distribution key is used for the individual items. In most cases, the costs are allocated according to the co-ownership share (MEA). Costs that can be precisely determined by meters and allocated to the residential unit are apportioned according to actual consumption.

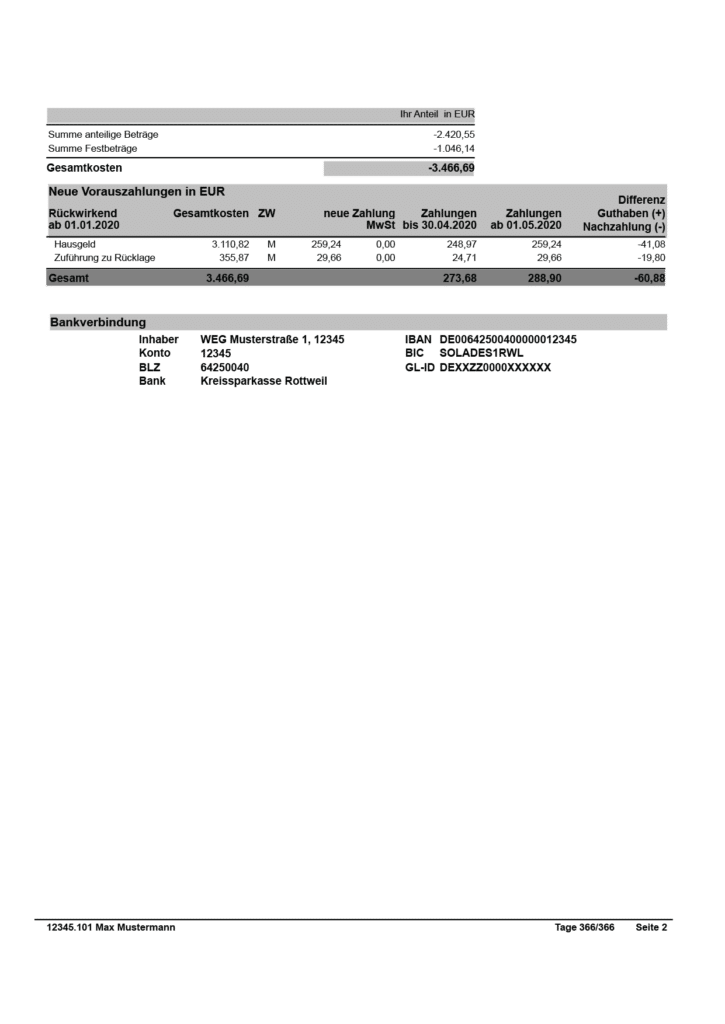

Your new advance payment and the retroactive debit position using an example:

1. total costs to be distributed

The planned annual expenditure

This is the planned annual expenditure for the entire building, broken down by category (e.g. rubbish, water, repairs, etc.).

2nd key Total / Proportionate

The distribution key

If you live in a house with several parties, the costs are calculated proportionally for each flat to ensure a fair distribution. The criteria according to which this is done is based on the declaration of partition of your property.

Here you can see how many parts of the whole you have to pay. The distribution key may vary depending on the category of expenses.

3. apportionable costs

Costs which can be passed on to a tenant

In the sample business plan shown, we have estimated € 2,726.80 as annually apportionable operating costs. For the tenant, this corresponds to a monthly advance operating cost payment of € 227.23 (€ 2,726.80 / 12 months). At the end of the financial year, you will receive your income and expenditure statements from us so that you can settle with your tenant.

IMPORTANT: This is only a general classification of costs - which costs you can actually pass on to your tenant depends on the conditions negotiated with your tenants in your tenancy agreement.

4. non-allocable costs

Costs that cannot be passed on to a tenant

These are costs that are assessed for the management and maintenance of your property. Please note that these costs cannot be passed on to a tenant.

5. total (apportionable costs + non-apportionable costs)

I

In this item we have presented the addition of all planned expenses for the entire business year. The subdivision into "apportionable operating costs" and "non-apportionable costs" is a presorting of the costs that are subject to the legal regulations: "II. BVO" (Second Calculation Ordinance).

6. total costs (house fees + maintenance reserve)

The costs shown here correspond in total to the same costs as in point 5, however, the total costs must be shown separately in "house fees" and "maintenance reserve".

7. payments until 30.04.2020

Representation of the currently valid house charge amount (in the example € 273.68 until 30 April). The amount is based on the currently approved business plan.

8. payments from 01.05.2020

Representation of the future monthly house charge amount, based on the previous year's consumption (in the example € 288.90 from 1 May). If the business plan is approved by the owners' association in April 2020, the monthly house charge amount in this example will change as of 1 May 2020.

9. difference credit (+) / back payment (-)

Since the business plan is always decided retroactively to the beginning of the business year (in this example, to 01.01.), there is a so-called "retroactive debit position". This is the difference between the old and the new advance payment multiplied by the months in which the old house payment amount was paid:

This amount was underpaid/overpaid according to the new business plan for the previous months (until the newly approved business plan comes into effect) and will be debited/credited in one sum.

10. bank details

The bank details of your homeowners' association are shown here. The monthly house fees are to be paid into this account.